The Systems That Move Your City's Money

- May 10

- 4 min read

Your city collects billions of dollars a year. The systems that move it are older than the internet, held together by vendor contracts, and invisible until they break.

Imagine it is a Tuesday in May.

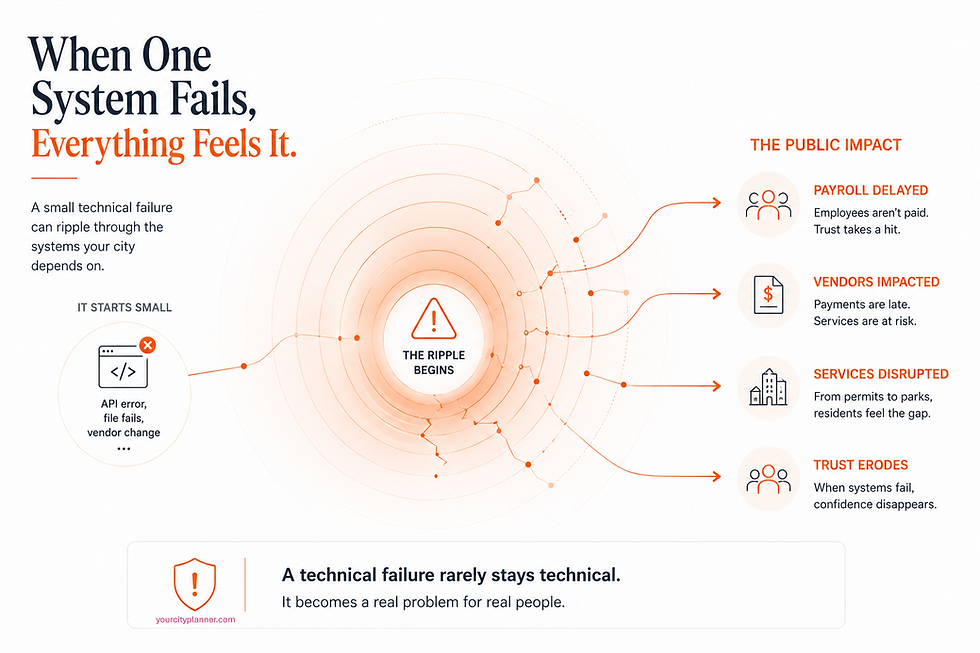

A mid-sized American city processes payroll on Thursdays. The vendor that handles its direct deposit file transfers has just been acquired. Over the weekend, the new parent company pushed what it described as a routine API update. Nobody flagged it as a breaking change. By Wednesday morning, the city's finance director learns the file will not transmit. Payroll is in 36 hours. There is no backup system. There is no fallback vendor on contract. There is a phone call with a technical support line in another time zone.

This has not happened in Alhambra or Marin County. But the conditions that would allow it to happen exist in both places, and in virtually every local government in the United States.

The infrastructure that moves public money is largely invisible, deeply dependent on a small number of private vendors, and almost entirely unknown to the residents whose trust it requires to function.

That is not an accident. It is the predictable outcome of a system that was never designed to be seen.

The Invisible Relationship

For more than two decades, the City of Alhambra relied on Bank of the West for its core financial operations: payroll, utility payments, parking citations, and daily deposits. The relationship had the comfortable inertia of infrastructure that simply works. Nobody called a press conference when ACH transfers cleared on time. Nobody issued a report when zero-balance accounts swept correctly at the end of the day. The system was invisible in the way that working systems always are.

Then Bank of the West was acquired by BMO in February of 2023. Service disruptions followed. By 2024, Alhambra's City Council was reviewing bids from competing banks and approved a five-year agreement with U.S. Bank to take over its depository, cash management, and check processing services.

The transition was procedural. It was also, briefly, clarifying.

What the process revealed was how much of the city's daily functioning depends on relationships nobody thinks about until they fail. Payroll timing, vendor disbursements, real-time cash visibility across multiple accounts: all of it flows through a single banking relationship, governed by a contract most residents have never read and managed by a department most residents could not name.

When the bank changed, the city had to specify, in precise terms, exactly what it needed. It was the first time in a generation it had been asked to do so.

The document that emerged is not glamorous reading. It describes a system of zero-balance accounts, Positive Pay controls, daily balance reporting, and transaction monitoring. It requires the bank to match every outgoing check against an authorized issue file before clearing it. It specifies how many deposits the city processes each month, how funds must be swept between accounts, and what happens when a stop payment is requested.

Every requirement in it describes something the city cannot function without.

What it does not describe is what happens when the vendor fails to deliver any of it.

How the System Grows

Alhambra shows what happens when the system falters. Marin County shows how the system evolves.

North of San Francisco, the Marin County Department of Finance manages something most residents would find surprising: a pooled investment portfolio averaging over $2.72 billion in 2026, supporting not just county operations but more than 90 school districts, special districts, and other public entities across the region.

Each of those entities has its own timing, its own obligations, its own demands on cash. The county is not managing a single balance sheet. It is managing a shared financial system for much of the public sector in one of the wealthiest counties in the country.

To do that, it accepts payments through channels that rarely touch a single platform: in person, online, by mail, through lockboxes, ACH transfers, wire transfers, and merchant card networks operated by FIS, Stripe, PayPal, and Square.

Every transaction, regardless of where it originates, must be reconciled back to the county's enterprise resource planning system by the end of the day. Daily reconciliation, for high-volume accounts tied to tax collections and merchant activity, is not a best practice. It is a contractual requirement.

This is not a system anyone designed in a single moment. It is a system that accumulated over decades, as payment channels multiplied, vendors proliferated, and the definition of what a government treasury does quietly expanded.

Marin's finance department recently underwent its first leadership transition in more than 30 years. In 2022, the county appointed Mina Martinovich as finance director after more than a decade inside the department, an internal promotion that reflected continuity as much as change. The systems are familiar to the new director. The scale and interdependency they now have to manage are something else entirely.

The county's 2026 request for proposals for banking services is, on its surface, a procurement document. In practice, it reads like something else: a forced inventory of every system the county depends on, laid out in technical language and contractual terms.

The Conditions for Failure

The public has no framework for understanding what it is trusting when it trusts a city to manage money.

The interaction is designed to feel simple and contained. You pay. The city receives. The service continues.

What that moment conceals is a network of private relationships, vendor contracts, and software dependencies that no elected official has fully mapped and no audit report fully captures.

That network does not fail often. Most of the time, payroll files transmit, reconciliations close, and the cash position is exactly where the finance director expects it to be.

In Alhambra, a bank acquisition forced the city to articulate, in writing, exactly what its daily operations require. In Marin County, a procurement cycle forced a similar accounting at a scale that encompasses dozens of public agencies and billions in pooled funds.

Both documents are records of how much depends on systems that almost nobody watches.

The conditions for failure are not exceptional. They are built into the structure.

When a vendor is acquired, when an API changes, when a banking relationship that has functioned for decades suddenly cannot, there is often no fallback. There is a phone call. There is a workaround. There is a finance team doing, quietly and without recognition, the work that keeps the system from becoming visible in the worst possible way.

The front end makes it look easy.

The system behind it is anything but.

Comments