- Apr 5

- 4 min read

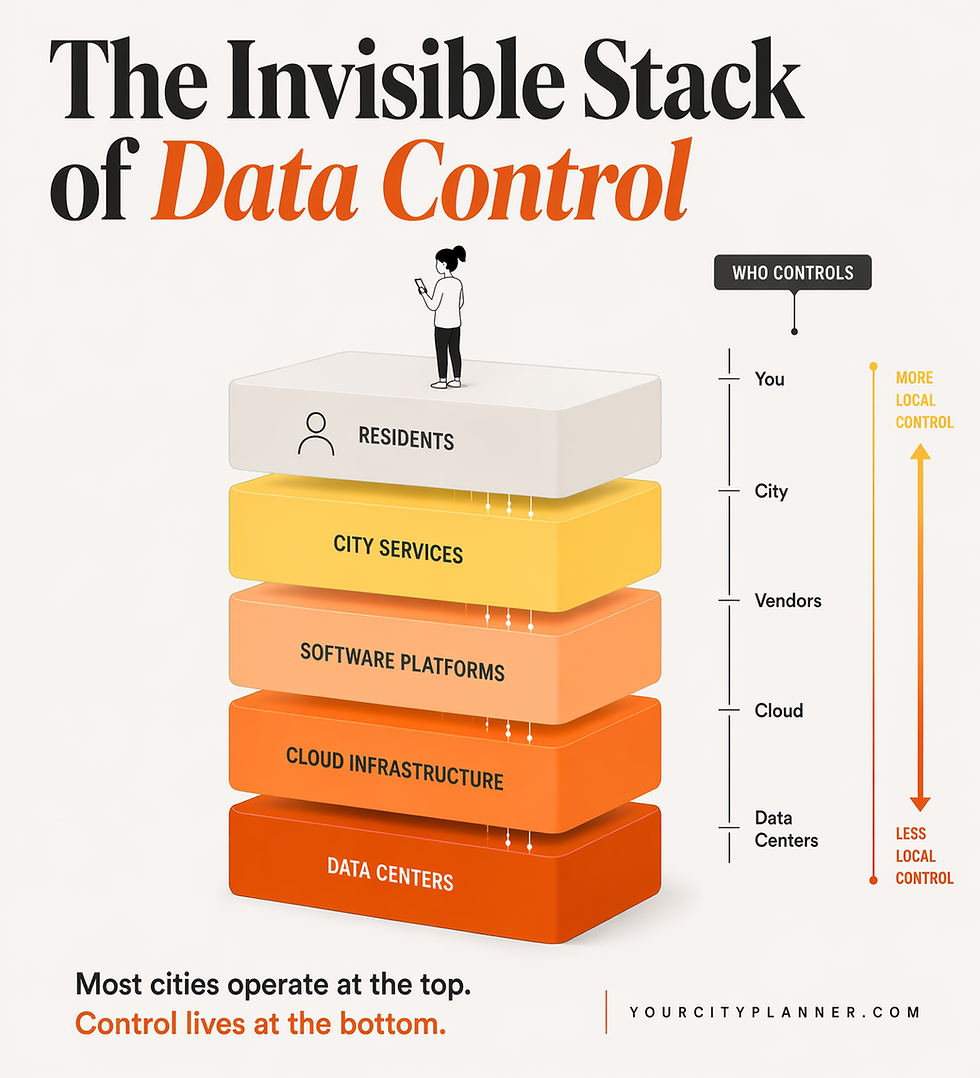

You pay your water bill, call 311, apply for housing help. Your information travels somewhere. The question is where, and who's in charge when it gets there.

If you asked where your city's data lives, City Hall would be the obvious guess. It's where decisions are made, where records are kept, where government, in theory, governs. But increasingly, your city doesn't actually run from City Hall.

Every time you pay a bill online, check a transit app, apply for housing assistance, or call 311, your information isn't staying within the walls of local government. It's moving through a web of cloud platforms, software vendors, and data centers; often owned by companies far outside your city, and sometimes far outside your country.

This is what people mean when they talk about digital sovereignty. Strip away the jargon and it comes down to a deceptively simple question: Who is actually in control of the systems your city depends on?

It's not just about where data is stored, though that matters. It's about who designs the architecture, who maintains the infrastructure, who sets the terms; and who holds leverage when something breaks, scales, or needs to change. Increasingly, the answer is not the city.

What makes this moment different is that digital infrastructure is no longer abstract. It has a physical footprint. It draws power. It consumes water. It competes for land. It shows up at zoning hearings and community meetings, not just in IT departments.

At the city level, digital sovereignty often looks like a planning decision disguised as a technical one. Do you approve a new data center that promises jobs and tax revenue, but will draw as much electricity as a small neighborhood? Do you outsource systems to global providers for speed and cost savings, or invest in building internal capacity that may be slower but offers real control?

These are no longer back-office decisions. They are infrastructure choices, the kind cities used to make about roads and water mains.

At the state level, the conversation shifts to resources. As demand for computing power grows, so does demand for energy. States are beginning to face genuine tradeoffs: who gets access to power when supply is constrained? Housing, manufacturing, and small businesses, or large-scale data operations that promise long-term economic growth?

Meanwhile, states are quietly becoming regulators of the digital layer itself. Data privacy laws, procurement rules, and utility policies all shape how much control residents actually have over their own information; even if most people never see those decisions being made.

At the national level, the tone sharpens. Governments talk about security, independence, and competitiveness. Some require that data be stored within their borders. Others invest heavily in domestic infrastructure. Many do both, and then quietly strike partnerships with the same handful of global tech companies they're supposedly guarding against.

Here's the part that rarely gets said out loud: even as governments push for "sovereignty," much of the infrastructure is still designed, financed, and operated by a relatively small group of firms, most of them based in the United States.

So you get a layered, sometimes contradictory dynamic. A country wants control over its digital future. A state wants to manage its resources responsibly. A city wants investment, innovation, and operational efficiency. A community wants to understand why a new building is using so much power and water.

And somewhere in the middle, a data center gets approved.

This isn't quite digital imperialism. But it isn't entirely neutral, either. It's a negotiation. One that plays out through contracts, zoning approvals, incentive packages, and infrastructure investments. And like most infrastructure negotiations, the benefits and burdens are not evenly distributed.

The companies that build and operate these systems gain scale, market share, and long-term contracts. Cities gain access to tools and capabilities they couldn't build on their own. Residents get faster services, more seamless experiences, and new forms of access. But control becomes more diffuse. Dependencies deepen. And the ability to change course, or even fully understand the system, becomes more complicated.

Here's what cities often miss about their own position: they have more leverage than they think.

Cities don't need to own the cloud to shape it. But they do need to understand where they sit within it. Because cities are not passive users of this system, they are hosts. They provide the land, the permits, the workforce, the energy grid, and the political approval that makes this infrastructure possible. They sit at the application layer, where demand is created and felt most directly.

The real issue is whether cities use that leverage, or keep giving it away.

The decisions being made right now, often quietly, in planning departments and procurement offices and utility commissions, are setting the terms for how cities will function in a digital economy for decades. For most residents, this will remain invisible, until it isn't. Until a system goes down. Until costs spike. Until access changes.

Infrastructure is always political. The only thing new is that most people don't realize this is infrastructure. They assume the system is controlled, that someone responsible is holding the keys. Cities are. The question is whether they've noticed they've been loaning them out.